The European mobile market is experiencing a notable shift driven by price sensitivity. This is giving a boost to low-cost players and forcing traditional companies to develop new strategies to address churn, according to the "Oliver Wyman Global Consumer Survey 2024: Connectivity."

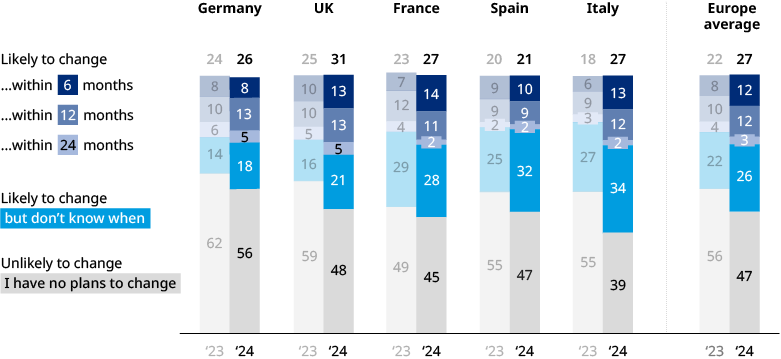

Over the next two years, 27% of European consumers are likely to change their mobile operator, marking a 5 percentage point increase year-over-year, according to the survey, which polled more than 7,000 consumers. This trend is particularly pronounced in Italy, where the likelihood of switching operators has surged by 9 percentage points to 27%, and in the United Kingdom, where it has increased by 6 percentage points to 31%.

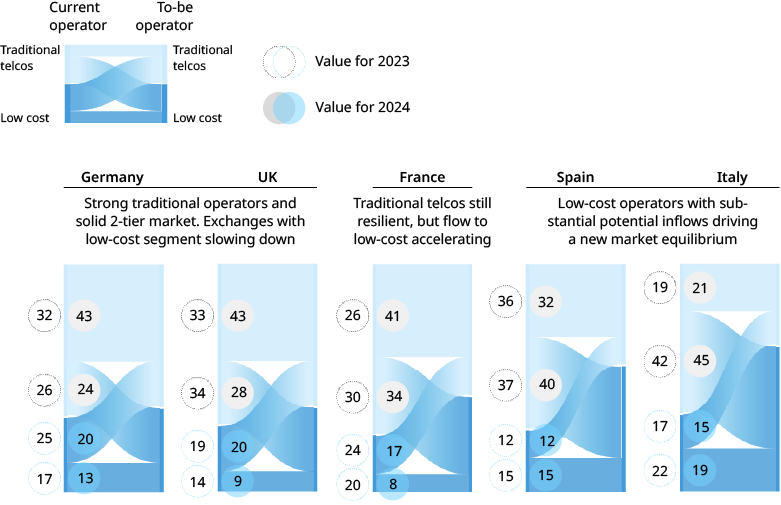

Traditional telecom companies are losing nearly half of their customers to low-cost competitors. However, the dynamics of this shift vary across different markets. In Spain and Italy, the migration to low-cost operators is accelerating, while in Germany and the United Kingdom, traditional operators are showing improved resilience against this trend.

Intentional churn is on the rise for fixed-broadband operators as well. Approximately 25% of European consumers are likely to change their fixed-line operator in the next two years, an increase of around 4 percentage points year-over-year. Network speed and pricing ranked as the top reasons for consumers making a change. Fiber-to-the-home (FTTH) availability and consumer interest are expanding across Europe, with Germany showing a notable interest increase of 19 percentage points year-over-year, indicating a growing demand for high-speed internet connections.

The push for fixed-mobile convergence (FMC) is stagnating in several key markets. In the United Kingdom and Germany, FMC is not significantly influencing trading dynamics, while in Spain and France, the market appears to be saturated. Only in Italy is FMC being actively promoted. Consumers' expectations of telecom companies are evolving, with a focus on connectivity and entertainment. There is growing skepticism about telecoms' ability to consolidate non-telecom household services, questioning their right to play in these areas.

Brand power battle between traditional and low-cost operators

Traditional carriers continue to dominate when it comes to brand awareness, but low-cost companies are catching up. However, in the United Kingdom and Italy, brand power is converging between traditional and low-cost operators. In every market, local champions — whether low-cost or local challengers — are emerging with brand perceptions as strong as those of well-established traditional brands. What is more, in most countries, a low-cost brand ranks among the top three brands, except in the United Kingdom. They are gaining more loyalty from customers as they report a strong, sometimes stronger, attachment compared to those with traditional brands. That makes preventing churn even more important for traditional carriers.

%20a.png)

Non-clients tend to have a negative perception of low-cost players, especially in France and Spain, while low-cost customers in Spain, France, and Italy have a strong brand perception of their operators. The United Kingdom remains an exception. FMC clients generally have a stronger brand perception, except in Spain, where FMC is commoditized, and in the United Kingdom, where FMC is regressing.

As the European mobile market evolves, it’s clear that the future belongs to those who can adapt and innovate. Traditional carriers must rethink their strategies and embrace change. The key to success lies in understanding the unique dynamics of each market and crafting tailored plans that resonate with the local consumer base.